X

Research source

However, the lender must agree to the assumption of any loan. If you happen to hold a loan and can’t get someone to assume it, then consider other options.

Applying to Assume a Loan

Ask your lender if this is an option. Not all lenders will let someone assume a car loan. For this reason, the person who holds the car loan should call up the lender and ask.

Pull credit scores. In this transaction, the person trying to assume the loan will need to get their credit checked. This credit score will largely determine whether they can assume the loan and at what interest rate. You can get credit scores in the following ways: Look on your credit card statement. Many credit card issuers provide free credit scores. Also look at your online account. Use a free online service, such as Credit.com. Some online companies charge, so make sure to use only a free service. Buy your FICO score from myfico.com. Meet with a credit or housing counselor. They should be able to get your credit score for free. Be careful, as there are many versions of your credit score. Be sure to ask lenders what model they use.

Complete an application. The person looking to assume the loan will need to fill out an application with the lender. The application will ask for financial information, because the lender must be confident they can pay back the loan.

Get a cosigner. The potential buyer’s credit might not be strong enough to get the lender to approve the loan’s assumption. In that case, he or she might need a cosigner. This means that a second party will be responsible for the loan in a failure to make payments. Of course, a potential buyer might not need to assume a loan if they have a cosigner. Instead, they can get their own car loan directly.

Wait for approval. The approval time will vary. The application might be approved immediately or might need a couple of weeks for a decision. The applicant should contact the lender if they haven’t heard anything after a couple of weeks.

Completing the Assumption

Analyze the contract. A potential buyer who is trying to assume a loan should make sure to understand everything fully before signing the agreement. Pay particular attention to the monthly payment amount and the due date. A first payment might be due very soon. If you’re assuming a loan, ask about anything you don’t understand and meet with a lawyer if necessary. Be sure also to check the loan’s balance and term and that it is no longer or higher than the person you are assuming it from has told you. You can obtain a referral to a lawyer by contacting your local or state bar association.

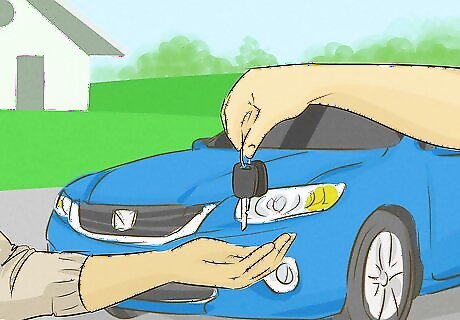

Sign paperwork. The buyer will sign their contract. The seller will then need to sign paperwork to transfer the title and the bank’s lien to the new owner. The lien will stay on the car until the car loan is paid off entirely.

Obtain insurance. If you’re assuming a loan, you can’t take possession of the car until you get insurance. Contact an insurance agent to find a policy and remember to provide the bank with proof of your insurance. Try to get at least three quotes so that you know you’re getting a competitive rate. If you’re the former owner of the car, you’ll need to cancel your insurance policy. There’s no reason to keep making payments.

Register the new car. Car registration requirements differ somewhat depending on the state. Contact your state’s DMV to find out the process for transferring a title and registering the car. You will also have to pay applicable taxes and fees at the time of registration.

Start making payments. Make timely payments each month if you’re assumed the loan, otherwise your car might be repossessed. If you run into financial trouble, call the lender and ask if they can help you.

Considering Other Options If You Can’t Transfer Your Loan

Talk to the lender. Car owners who are unable to make payments have other options besides transferring their loan. Talk to your lender. Many are happy to let borrowers miss a payment and add it to the end of the loan. You’ll pay more in interest, but a short break might allow you to catch up on your loan. Find your lender’s contact information on your monthly statement. Have a reason why you can’t make the payment. For example, you might have had a medical emergency that used up your extra money that month.

Tap a home equity line of credit. A home equity line of credit (HELOC) is like a credit card. You’re given a line of credit, and you make monthly payments while being charged interest on the balance. You might be able to move the balance of your car loan to a HELOC. This way, you can keep your car. One huge pitfall is that you put your home at risk if you can’t make payments. However, this might be less of a concern if you don’t owe much money. Your HELOC’s interest rate is also variable, so you might pay more in interest than you would on the car loan. You should talk to a lender to see if HELOC interest rates would benefit you.

Ask a friend or family member for a small loan. Keep on top of your car payments by asking someone close to you if you can borrow money. They might be willing to lend to you with little or no interest, which will help you manage your car loan while you straighten out your finances.

Trade in your car. Buying a new car might be the last thing you want to do. However, it can benefit you if you trade in for a much cheaper car. Try to get the dealership to give you trade-in credit equal to the amount you have left on your loan. For example, if you owe $5,000 on the car, try to get the dealer to give you $5,000 in trade-in credit. Also check the loan terms for your new car. Ideally, you’ll have a much lower monthly payment that you can afford.

Sell your car. If all else fails, you can still sell your car. You’ll need the lender’s permission to sell since they have a lien on the car, which can limit the pool of people willing to buy it. However, if you find a buyer, you can hold the sale at the bank where you have a loan. You’ll pay off the remainder of your loan, and the bank can transfer the title at the same time.

Comments

0 comment